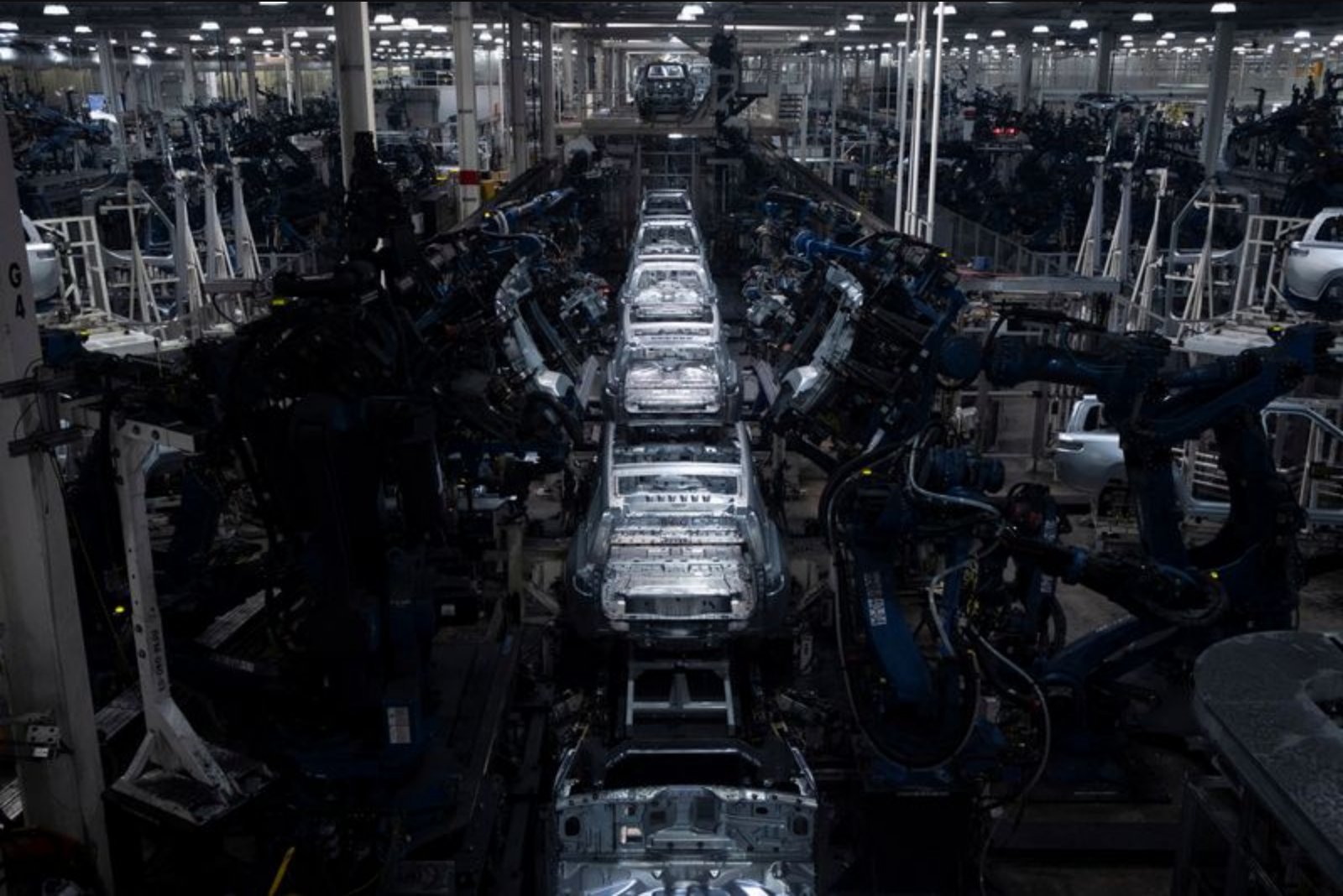

New orders for key U.S.-manufactured capital goods jumped markedly in March, producing the largest monthly increase in almost six years and underscoring robust equipment spending by businesses that helped support growth in the first quarter. Shipments of those goods also rose at a solid pace, according to Commerce Department data.

At the same time, a separate Commerce Department release showed the goods trade deficit widened sharply last month amid strong import growth. However, the anticipated negative effect of that shortfall on gross domestic product was likely tempered by a sizable increase in business inventories. The Commerce Department is scheduled to publish its advance estimate of first-quarter GDP on Thursday.

Economists linked the surge in equipment orders to an ongoing wave of investment in artificial intelligence infrastructure and data center construction, activity that has supported manufacturing even as tariffs on some imports remain in place. They also pointed to a flurry of orders placed in March in anticipation of higher prices and potential shortages related to the U.S.-Israeli war with Iran as a likely contributor to the outsized rise in so-called core capital goods bookings.

"The stunning degree of strength during a month when firms would have had valid reason to be cautious attests to the substantial energy in business investment that was bottled up last year due to policy-related uncertainty," said Stephen Stanley, chief U.S. economist at Santander U.S. Capital Markets.

Non-defense capital goods orders excluding aircraft - a closely watched proxy for business investment - increased 3.3% in March, the Census Bureau reported. That was the largest month-over-month gain since June 2020 and followed an upward revision to a 1.6% increase in February.

Economists polled by Reuters had expected a 0.5% rise in these core capital goods orders after a previously reported 0.7% advance in February.

The broad advance in orders was driven in part by computers and electronic products, which surged 3.7% on strong demand for communications equipment. There were also notable increases in orders for machinery, electrical equipment, appliances and components.

Shipments of core capital goods climbed 1.2% in March after rising 1.3% in February. Those shipments are inputs to the business spending on equipment component that feeds into the GDP calculation, so the jump has direct implications for the advance GDP estimate.

Analysts expected that stronger equipment investment would help offset signs of a further slowdown in consumer spending during the quarter.

Orders for durable goods - items designed to last three years or more, from household appliances to aircraft - rebounded 0.8% in March after a 1.2% decline in February. The gain was supported by a 0.8% increase in orders for transportation equipment.

Financial markets registered a reaction to the data. Stocks on Wall Street traded lower, the dollar strengthened against a basket of currencies, and U.S. Treasury yields rose following the reports.

Goods trade and inventories

In a separate Census Bureau report, the goods trade deficit widened 5.3% to $87.9 billion in March. Imports of goods rose $9.6 billion to $299.3 billion, driven in part by an 11% surge in motor vehicle imports. There were also solid month-over-month increases in imports of food, consumer goods, capital goods and industrial supplies.

Some of the uptick in imports flowed directly into inventories. Wholesale inventories increased 1.4%, while retail stocks rose 0.7% in March.

Goods exports climbed $5.2 billion to $211.5 billion in March, with increases in shipments of food, motor vehicles, capital goods and industrial supplies, which include petroleum. Exports of consumer goods, however, declined 7.5% in the month.

Economists noted that the Middle East conflict could boost U.S. goods exports in coming months, given the country is a net oil exporter, but the reports for March already showed an expansion in exported goods in several categories.

Implications for GDP and outlook

The combination of strong core capital goods shipments and rising inventories pointed to a possible upside surprise to economists' consensus for GDP growth in the January-March quarter. A Reuters survey of economists forecast that GDP grew at a 2.3% annualized rate in the quarter, up from a 0.5% gain in the fourth quarter.

Signs of robust business investment, even after accounting for some inflationary effects, supported expectations that the Federal Reserve would keep its benchmark overnight interest rate in the 3.50% to 3.75% range and likely hold it there for an extended period.

Housing mixed; residential investment under pressure

Housing data released alongside the manufacturing and trade reports were mixed. Single-family homebuilding rose to a 13-month high in March, but that improvement appeared to reflect builders catching up after earlier weather-related disruptions rather than a durable upswing.

Single-family housing starts, which make up the majority of new home construction, surged 9.7% to a seasonally adjusted annual rate of 1.032 million units in March, the highest level since February 2025. On a year-over-year basis, single-family starts were up 8.9%.

At the same time, permits for future construction of single-family homes fell 3.8% in March to 895,000 units and were down 7.9% from a year earlier. Homebuilding has faced headwinds from tariffs on imported inputs, including lumber and vanity cabinets, and mortgage rates remain elevated, constraining some buyers.

Economists surveyed believe residential investment - which includes homebuilding - contracted for a fifth straight quarter in the January-March period.

"We expect housing starts to fall again in April and May as the uncertainty and higher costs brought by the war in the Middle East cause both builders and potential buyers to take a step back in the near-term," said Ben Ayers, senior economist at Nationwide.

Bottom line

March's outsized increase in core capital goods orders and solid shipments point to a notable resurgence in equipment investment that could lift first-quarter GDP above earlier estimates, even as the widening goods deficit and mixed housing signals highlight areas of uncertainty. Inventories rose alongside imports, suggesting some imported goods were being held rather than consumed, which could dampen the trade-related drag on growth when the advance GDP estimate is released.