Hook / Thesis

I was early on Applied Optoelectronics (AAOI) when the company’s traction in high-speed data-center optics first showed up in revenue prints. The narrative — VCSEL-driven 800G short-reach transceivers selling into hyperscalers and cable operators — has progressed from proof-of-concept to volume shipments. That evolution has driven a dramatic re-rating: the stock has moved from a 52-week low near $9.71 to trading above $100.

That move leaves an actionable middle ground. I own the story and still view AAOI as a beneficiary of AI-driven interconnect demand, but today's price embeds lofty growth expectations. My trade is a disciplined, mid-term long sized to respect both upside from continued 800G adoption and the real risk that expectations get trimmed.

What the company does and why the market should care

Applied Optoelectronics designs and manufactures optical communications products: laser diodes, photodiodes, related modules and the transceivers used inside data-center racks and cable infrastructure. The company's recent relevance is tied to two fundamental drivers:

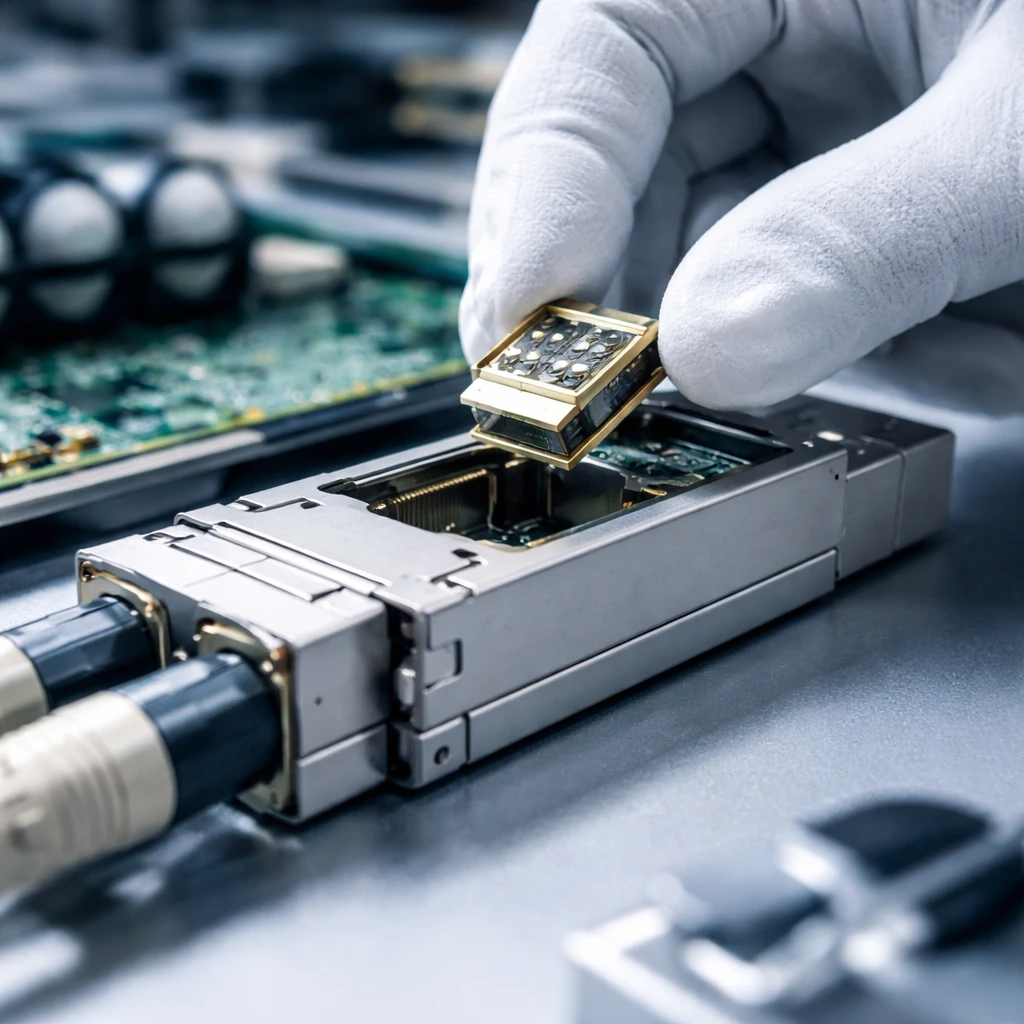

- AI data-center interconnects - Customers are deploying 800G transceivers for high-bandwidth, short-reach links inside AI clusters. AAOI's VCSEL-based 800G OSFP 2xSR4 product is directly aimed at that market. The company publicly showcased that product at ECOC on 09/29/2025 and later announced first volume shipments to a major hyperscaler on 06/11/2025.

- Cable and access networks - AAOI continues to sell into FTTH and cable TV markets, cushioning cyclicality from hyperscale purchases and improving the overall revenue profile.

Investors should care because these end markets are structurally expanding: AI deployments are driving demand for more high-speed links per rack, and large cloud builds (including new data-center footprints) create repeatable, high-volume orders. That dynamic is visible in the reported growth: Q3 2025 revenue of $118.6M versus $65.2M year-over-year is an explicit example of the company's recent scaling.

What the numbers say

| Metric | Value |

|---|---|

| Current price | $103.215 |

| Market cap | $7.76B |

| 52-week range | $9.71 - $110.00 |

| Price-to-sales | 12.62x |

| EV / Sales | 12.53x |

| Free cash flow (recent) | -$353.6M |

| Current ratio | 2.59 |

| Average daily volume (30d) | ~6.36M |

| RSI (short-term) | ~85 (overbought) |

Two relevant technical and market signals: first, the stock's short interest remains meaningful (recently ~10.6M shares with days-to-cover around 2.1), which can accentuate swings; second, momentum indicators are stretched (RSI ~84.9) even as MACD shows bullish momentum. Volume has expanded - today's print is 21.4M versus a 30-day average of ~6.36M - indicating real interest and fast repositioning by institutions and traders.

Valuation framing

At a market cap of roughly $7.76B and P/S ~12.6x (EV/Sales ~12.5x), AAOI trades like a high-growth capital equipment name rather than a mid-cycle component supplier. That multiple is justifiable if revenue growth stays in triple digits or gross margins expand materially as 800G adoption scales. The company has demonstrated rapid top-line growth (Q3 2025: $118.6M vs $65.2M YoY; reported nine-month revenue growth of ~115% in 2025), but the business still shows negative earnings (EPS negative and free cash flow recently negative ~$353.6M). In short, the stock is priced for continued execution and margin improvement.

Catalysts to watch (2-5)

- Continued volume shipments to hyperscalers - incremental orders or multi-quarter purchase cadence would validate the 800G TAM conversion.

- New design wins announced publicly or at trade shows - public wins can act as re-rating events.

- Large cloud expansion plans (e.g., new data-center builds) that name AAOI as a supplier or imply incremental optical demand.

- Improvement in operating leverage - signs that gross margins and free-cash-flow trajectory turn positive across quarters.

Trade plan - concrete and actionable

My trade is a mid-term buy: enter a position using a limit order at $97.00. Place a stop loss at $88.00. Target $140.00 as the primary take-profit. Time horizon: mid term (45 trading days). Here’s the reasoning:

- Entry $97.00 - this is a pullback entry inside recent intraday ranges (today's low was $93.78), giving a better risk entry than buying at the highs near $110.

- Stop $88.00 - sits below the intraday swing low and provides a clear signal that demand has weakened. If price breaches $88 on volume, the thesis of durable hyperscaler traction is likely in question.

- Target $140.00 - a 44% move from the $97 entry. This target reflects a scenario where the company confirms follow-on volume shipments, margins improve modestly, and market multiple holds. It’s also a realistic near- to mid-term technical target if momentum continues and shorts cover.

- Horizon - mid term (45 trading days). I expect one or two meaningful catalysts or quarter-to-date trading updates to arrive in this window; either will allow us to re-assess. If AAOI reports sustained order flow or margin improvement within this window, I would hold for higher targets; if not, I will trim or exit at the stop.

Position sizing and risk management

This is a volatile name that can gap on news. Limit position size to an amount where the stop-to-entry loss equals no more than 1-2% of portfolio equity for retail sizing. If you are more aggressive, scale in using staggered entries (e.g., half at $97 and half lower), but do not chase at $110 without a clearly defined risk level.

Risks and counterarguments

Below are the major risks that could invalidate the trade or produce outsized losses. I include at least one counterargument for balance.

- Valuation risk - The company trades at P/S ~12.6x and EV/Sales ~12.5x. That pricing requires sustained, rapid revenue growth and margin improvement. If growth slows or margins fail to expand, multiple compression could lead to sharp downside.

- Profitability and cash flow - EPS is negative and free cash flow is negative roughly $353.6M. Continued cash burn or the need for dilutive financing would be a material negative and could compress equity value.

- Concentration/counterparty risk - A meaningful portion of near-term revenue is tied to a small number of hyperscalers. If a large customer delays purchases or switches suppliers, revenue and margin forecasts could suffer.

- Technical squeeze and volatility - Elevated short interest and high intraday volume create the potential for violent moves both up and down. That makes strict stops essential.

- Macro / policy disruptors - Tariff decisions, supply-chain constraints or sudden capex slowdowns at cloud providers could reverse the growth narrative quickly.

- Counterargument: Some investors will say the stock is already a runaway winner and therefore too risky on valuation grounds. That’s fair. However, large-cap institutional buys (e.g., a 1492 Capital purchase of ~215,987 shares on 02/24/2026) and multiple design-win announcements suggest the demand signal is not purely speculative. If revenue cadence remains strong and management shows path to positive FCF, the current multiple can be rationalized.

What will change my mind

I will materially reduce conviction (and likely exit) if one or more of the following occur within the mid-term horizon:

- Management discloses a meaningful slowdown or cancellation of hyperscaler orders.

- Quarterly revenue growth meaningfully decelerates from the recent ~115% nine-month growth pace without offsetting margin improvement.

- Free cash flow remains deeply negative with no credible path to breakeven and the company indicates the need for dilutive financing.

Conclusion

I remain constructive on AAOI's end-market opportunity: AI-driven bandwidth demand and 800G adoption are real forces, and the company has moved from R&D into volume shipments. But the stock has also moved fast, and the balance between execution upside and valuation risk is delicate.

For traders who agree with the thesis but want discipline: use the plan above - buy at $97.00, stop at $88.00, target $140.00, and evaluate after mid-term catalysts within ~45 trading days. Keep position sizes conservative, respect the stop, and watch order cadence and margin commentary closely. If AAOI proves durable order flow and positive free-cash-flow trajectory, I will consider raising targets or moving to a position trade; if not, the stop is there to protect capital.

Key operational readouts in the coming weeks - shipment cadence, public design wins and margin expansion - will determine whether this rally has staying power or is a near-term repricing that needs to be faded.